In my mind, the best example of applying MMT, while juggling structural inflation and balance of payments constraints, is India since 1980. Before I delve into the main story, a 5-minute tour of modern Indian economic history.

Until 1980, India was stuck in what was pejoratively termed the "Hindu rate of growth" by economist Raj Krishna. It is now widely acknowledged that growth took off in 1980, although in popular commentaries 1991 is seen as the watershed year. The chart below and more sophisticated tests show that there was a trend break in growth around 1980.

However, there is considerable debate about the causes of the growth takeoff in the 1980s and whether it was sustainable. Many, perhaps most, economists believe that the 1980s growth was unsustainable, fueled by a rapid increase in government spending and deficits. The deficit-spending spree led to a steep rise in government debt, rising inflation, and a worsening current account deficit and foreign currency debt culminating in the 1991 BOP crisis. The major dissenters from this view are the current CEA, Arvind Subramanian, and his co-author Dani Rodrik, who argued that the 1980s growth was not driven so much by old-fashioned Keynesian stimulus but by a more business-friendly attitude of the Indira Gandhi government.

Post-Keynesians predictably have a different take on the entire growth take-off story. Kevin Nell has a few papers arguing: 1) India was demand constrained in the 1952-1979 period, and fiscal expansion took the economy closer to potential; 2) India faced a BOP constraint on growth that was significantly eased by the surge in exports post 1991; 3) the post 1991 export surge may have had a demand-side explanation. I largely agree with Nell's analysis, although I disagree with him (and others) about how much the 1991 BOP crisis was the result of "unsustainable" growth in demand.

I am going to look at the India experience from the MMT angle of government deficits and sector financial balances. Since 1980, India has in effect followed the prescriptions of functional finance--generally pursuing fiscal and monetary policies that support high growth but turning attention to inflation-fighting and BOP concerns when needed. This strategy has actually allowed India to address poverty alleviation while delivering solid returns on capital (India has been one of the best in delivering dollar-based returns over the past 25 years).

Evolution of Fiscal Deficits

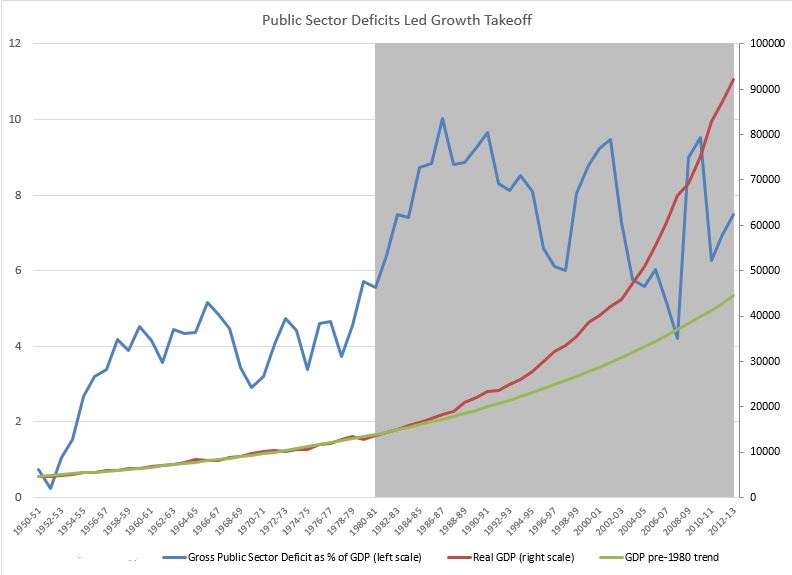

One of the most striking things about India was that the gross public sector deficit (the public sector includes the central and state governments, departmental enterprises, and public sector corporations; deficits are gross investment less gross saving) scaled to GDP has been permanently higher since 1980 (chart below). Only in one year, 2007-2008, did it fall below the peak of the pre-1980 range; in every other year since 1980, it has been higher than the peak of the pre-1980 range. Yet, this period has also coincided with the takeoff in the India's GDP from the previous Hindu rate of growth. One cannot establish that the deficits caused the growth ( I am working on a paper that seeks to establish this more formally--anyone interested in collaborating please email me), but such a chart has to warm MMT cockles.

At the same time, whenever faced with rising inflation, the government has throttled back. As the chart below shows, deficits have contracted whenever inflation has accelerated. This is straight out of the MMT playbook. The glaring error was in 2010, when deficits remained high despite surging inflation.

Meanwhile, government debt scaled to GDP has been relatively stable for nearly 30 years, except for the brief run-up in 2002-2003. Monetary policy may not have completely followed the prescriptions of functional finance, which is to conduct interest policy with a view to making debt sustainable, but it sure appears to have been doing something close.

One other point that supports the MMT view that government deficits are different from an expansion in money and credit brought about by private sector credit expansion. The Indian government nationalized 14 major banks in 1969 in order to make credit more widely accessible and to make "banks serve the needs of the nation." Nationalization appears to have been a factor in driving faster credit growth. M3 (which is a proxy for broad credit) scaled to GDP appears have had a trend break around 1969-1970, as the chart below shows. Yet, neither did GDP pick up nor did poverty decline in the 1970s.

The 1970s also illustrate the importance of supply side reforms to go along with demand push. In the 1970s, the government had terrible policies that hobbled the supply side: 1) harsh implementation of the monopolies and restrictive trade practices act that made plant sizes uneconomical and licenses hard to obtain, and 2) draconian controls that squelched imports of needed capital goods. Thus, inflation soared (of course, the oil shock of 1973 and poor monsoons aggravated matters). In the 1980s and much more so in the 1990s, the government eased supply-side constraints, allowing demand push to result in higher growth. Only demand push without supply side reforms would have been dissipated in higher inflation as in the 1970s.

Growth has been the Biggest Factor Driving Down Poverty

India has made remarkable progress in reducing the poverty rate over the past 35 years. The biggest factor driving the decline in poverty is economic growth, as the chart below shows. There was very little progress made in reducing poverty until 1980 despite the plethora of so-called poverty alleviation programs.

Return on Capital has also been Solid

Since 1995, in dollar terms, Indian stock market returns have almost matched the S&P 500 and handily beaten the world and other emerging markets.

I have argued elsewhere that Indian equities have also outperformed gold since 1979. Lastly, India's public provident fund (PPF)--a tax-advantaged small savings vehicle fully guaranteed by the central government--has outpaced gold and provided modest positive, real returns.

In short, India has not treated capital too shabbily.

Until 1980, India was stuck in what was pejoratively termed the "Hindu rate of growth" by economist Raj Krishna. It is now widely acknowledged that growth took off in 1980, although in popular commentaries 1991 is seen as the watershed year. The chart below and more sophisticated tests show that there was a trend break in growth around 1980.

However, there is considerable debate about the causes of the growth takeoff in the 1980s and whether it was sustainable. Many, perhaps most, economists believe that the 1980s growth was unsustainable, fueled by a rapid increase in government spending and deficits. The deficit-spending spree led to a steep rise in government debt, rising inflation, and a worsening current account deficit and foreign currency debt culminating in the 1991 BOP crisis. The major dissenters from this view are the current CEA, Arvind Subramanian, and his co-author Dani Rodrik, who argued that the 1980s growth was not driven so much by old-fashioned Keynesian stimulus but by a more business-friendly attitude of the Indira Gandhi government.

Post-Keynesians predictably have a different take on the entire growth take-off story. Kevin Nell has a few papers arguing: 1) India was demand constrained in the 1952-1979 period, and fiscal expansion took the economy closer to potential; 2) India faced a BOP constraint on growth that was significantly eased by the surge in exports post 1991; 3) the post 1991 export surge may have had a demand-side explanation. I largely agree with Nell's analysis, although I disagree with him (and others) about how much the 1991 BOP crisis was the result of "unsustainable" growth in demand.

I am going to look at the India experience from the MMT angle of government deficits and sector financial balances. Since 1980, India has in effect followed the prescriptions of functional finance--generally pursuing fiscal and monetary policies that support high growth but turning attention to inflation-fighting and BOP concerns when needed. This strategy has actually allowed India to address poverty alleviation while delivering solid returns on capital (India has been one of the best in delivering dollar-based returns over the past 25 years).

Evolution of Fiscal Deficits

One of the most striking things about India was that the gross public sector deficit (the public sector includes the central and state governments, departmental enterprises, and public sector corporations; deficits are gross investment less gross saving) scaled to GDP has been permanently higher since 1980 (chart below). Only in one year, 2007-2008, did it fall below the peak of the pre-1980 range; in every other year since 1980, it has been higher than the peak of the pre-1980 range. Yet, this period has also coincided with the takeoff in the India's GDP from the previous Hindu rate of growth. One cannot establish that the deficits caused the growth ( I am working on a paper that seeks to establish this more formally--anyone interested in collaborating please email me), but such a chart has to warm MMT cockles.

At the same time, whenever faced with rising inflation, the government has throttled back. As the chart below shows, deficits have contracted whenever inflation has accelerated. This is straight out of the MMT playbook. The glaring error was in 2010, when deficits remained high despite surging inflation.

Meanwhile, government debt scaled to GDP has been relatively stable for nearly 30 years, except for the brief run-up in 2002-2003. Monetary policy may not have completely followed the prescriptions of functional finance, which is to conduct interest policy with a view to making debt sustainable, but it sure appears to have been doing something close.

One other point that supports the MMT view that government deficits are different from an expansion in money and credit brought about by private sector credit expansion. The Indian government nationalized 14 major banks in 1969 in order to make credit more widely accessible and to make "banks serve the needs of the nation." Nationalization appears to have been a factor in driving faster credit growth. M3 (which is a proxy for broad credit) scaled to GDP appears have had a trend break around 1969-1970, as the chart below shows. Yet, neither did GDP pick up nor did poverty decline in the 1970s.

The 1970s also illustrate the importance of supply side reforms to go along with demand push. In the 1970s, the government had terrible policies that hobbled the supply side: 1) harsh implementation of the monopolies and restrictive trade practices act that made plant sizes uneconomical and licenses hard to obtain, and 2) draconian controls that squelched imports of needed capital goods. Thus, inflation soared (of course, the oil shock of 1973 and poor monsoons aggravated matters). In the 1980s and much more so in the 1990s, the government eased supply-side constraints, allowing demand push to result in higher growth. Only demand push without supply side reforms would have been dissipated in higher inflation as in the 1970s.

Growth has been the Biggest Factor Driving Down Poverty

India has made remarkable progress in reducing the poverty rate over the past 35 years. The biggest factor driving the decline in poverty is economic growth, as the chart below shows. There was very little progress made in reducing poverty until 1980 despite the plethora of so-called poverty alleviation programs.

Return on Capital has also been Solid

Since 1995, in dollar terms, Indian stock market returns have almost matched the S&P 500 and handily beaten the world and other emerging markets.

I have argued elsewhere that Indian equities have also outperformed gold since 1979. Lastly, India's public provident fund (PPF)--a tax-advantaged small savings vehicle fully guaranteed by the central government--has outpaced gold and provided modest positive, real returns.

In short, India has not treated capital too shabbily.

India has also adopted another MMT favorite--job guarantee--in a limited way in the form of MNREGA. The present government has tried to ensure that MNREGA employment goes toward building assets in the form of rural infrastructure. (I am personally ambivalent about job guarantee.)

I am pretty sure that most Indian policymakers would be aghast to know that India has actually been following the prescriptions of MMT all along!