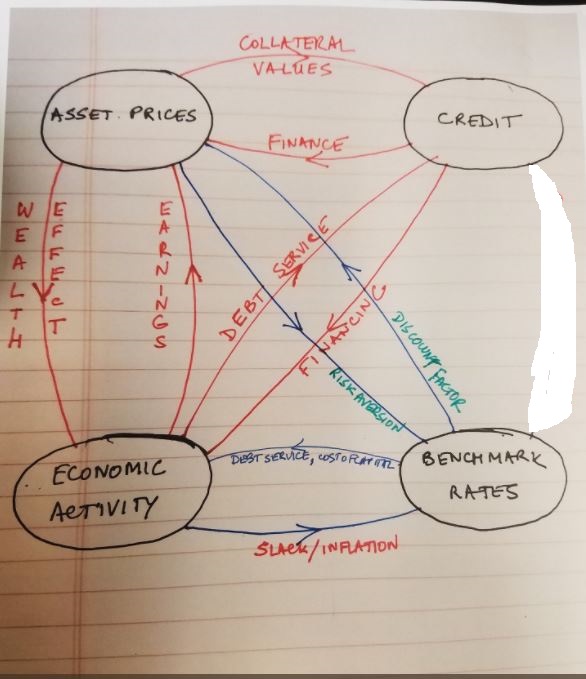

Inspired by this post by Edward Harrison, I sketched the diagram below to show the various feedback loops operating in the economy. Red arrows are positive feedback loops (destabilizing) and blue arrows are negative feedback loops (stabilizing), By no means is this a comprehensive rendering of all interactions in the economy, but it is good enough to illustrate monetary policy dynamics, the inherent instability of a system, and that a single interest rate that stabilizes the system is unlikely to exist.

Start with the bottom loop, which we can call the conventional view of the real economy. Economic activity picks up, slack diminishes, inflation rises, and the Fed hikes rates, which, in turn, increases the cost of the capital and debt-service costs and slows the economy. In this Wicksellian world of New Keynesian economics, there exists a single rate, the natural rate, that delivers stable economy growth with steady inflation.

Let us bring in credit. There is a positive feedback loop between credit and the economy. Greater availability of credit boosts the economy, and increased economic activity, in turn, supports debt-service and validates the credit decisions. The central bank usually does not interfere with the credit channel directly. In crises, central banks step in directly to provide liquidity to the credit markets. In theory, they have macroprudential tools to directly control credit markets. In practice, monetary policy assumes that the interest rate that stabilizes economic activity also stabilizes credit via debt service.

Finally, include the asset side of the economy. Now, there are three positive feedback loops: 1) between the real economy and credit, 2) between credit and asset prices, and 3) between asset prices and the real economy. There are two negative feedback loops--but the second one between monetary policy and asset prices is not directly operative to the extent the Fed eschews "targeting asset prices." So, essentially there is one negative feedback loop to stabilize the economy against three potentially destabilizing dynamics. In the perfect world of rational expectations and common knowledge, this is not a problem. If financial market participants bid up asset prices, Tobin's Q would go up. Firms would be incentivized to invest, which would then strengthen the economy, leading to higher interest rates and lower asset prices.

However, in the real world, the expectations of financial market participants can diverge from the expectations of business executives making capital spending decisions. So, if financial market participants take a rosier view of the future, they can bid up asset prices, but, to the extent business capital spending decisions are driven less by cost of capital and more by demand, business executives may see limited opportunity for fixed investment. In that case, the economy may remain tepid, the Fed will remain accommodative, supporting the asset price speculation. Moreover, to the extent the real economy has considerable slack, the Fed has the freedom to address financial market turmoil, or the Fed Put is closer to the money. In some ways, this describes the situation of the past several years. On the other hand, if the real economy is booming and/or inflation is high, the Fed, driven by real economy considerations, may be constrained in its willingness to pay obeisance to every market hiccup. The Fed Put would be further out of the money. For instance, in 2000, as the Nasdaq was plunging, the tight labor market prevented the Fed from cutting aggressively until it was too late. One could say the same in 2007--home prices were falling and the positive feedback loops from home prices to housing credit were beginning to look ominous--but inflation and still low unemployment prevented the Fed from aggressively cutting rates to resuscitate the housing market.

Suppose the system were somehow stable. Minskian meta-dynamics throws wrench. If the system is stable, then some participants on the margin will be encouraged to take a little bit more risk by extending credit to more risky borrowers, bidding up asset prices, and raising the credit-to-GDP ratio. The increased flow of credit will boost economic activity, forcing the Fed to tighten. However, note that the Wicksellian rate may now be too high to stabilize debt-service and the economy. When faced with rising inflation and increasing financial stresses, CBs have two choices, ignore inflation and focus on credit market stability or tackle inflation and allow a recession to occur. The idea that they can thread the needle--find a rate that delivers stable inflation and stable credit--is implausible in a Minskian world, unless there is heavy-handed and continuously evolving regulatory suasion (see this). Minsky in his own words:

Consider three separate episodes in U.S. history. First, 1966-67. Core inflation had surged from a sub-2% level in early 1966 to over 3.5% by late 1966. The economy was slowing but not enough to arrest labor market pressure. However, a severe credit crunch was developing. The Fed had two choices (I am grossly simplifying): ease policy to address the credit crunch or focus on inflation. The Fed eased, a recession was averted but inflation kept climbing thanks to which two people won Nobel prizes (one very, very undeserving in my opinion), and due to which the economics profession became madly obsessed with inflation.

Now consider 1990. The Fed had started easing in 1989 as bank and S&L failures were soaring and the economy was clearly weakening. But in early 1990, surging inflation stayed the Fed's hand despite growing financial stresses. Eventually, the Fed eased in the second half of 1990, but the economy was already in recession. In hindsight the inflation threat was a headfake, or was it? If the Fed had arrested banking sector problems, then credit flow would have not stopped, the economy would not have weakened, and in the absence of the magic expectations fairy, inflation likely would not have come down.

Let us now fast forward to 2008. Those who were "hawks" on the FOMC back then are being roasted right now on the 10th anniversary of the crisis. But consider the situation in mid June 2008 (not after Lehman had collapsed). Retail sales had rebounded strongly, ISMs were hovering near 50, real GDP growth had bounced back in the second quarter, and the global economy was solid. Not everything was fine--payroll decline was worsening for instance. Meanwhile, core inflation was accelerating and oil was skyrocketing toward $150. While financial stresses remained, the Fed had successfully engineered the absorption of Bear Stearns by JP Morgan and Countrywide by Bank of America, and the VIX, the TED-spread, and high-yield spreads had all declined.The Fed had already cut rates by 325 bps. So, is it such a blunder that the hawks resisted further easing in June-July? Without the advantage of hindsight, what makes easing of 1967 a blunder and not easing of 2008 a blunder too? Yet, monetarists in particular hold on to both views.

There was likely no right path: easing would have validated the hawks and not easing further validated the doves. As it were, the second path was chosen and the doves seem prescient, but like Schrodinger's cat, both views were right ex ante, but the whichever view was followed would have been proved to be wrong ex post!

(Let me be clear: my colleagues at the Levy Forecasting Center were expecting and betting on a deflationary collapse. Yet, we had the advantage of a financial-oriented systems dynamics view of the economy. The Fed was arguing from models of the real economy where balance sheets were an epiphenomenon.)

Many would consider the Fed's actions in 1990 and 2001 as successful instances of threading the needle in contrast to its policymaking in the 1960s and 1970s or 2008. Yet, the recessions of 1990-91 and 2001 had long-lasting effects. Matt Klein had an excellent piece on the early 1990s. The early 1990s was when the term jobless recovery was first coined. The Fed cut rates all the way into 1993--more than two years into the recovery. Federal deficits remained wide--recall Ross Perot's campaign? Growth was mediocre and productivity weak--Krugman called it the age of diminished expectations. It was not until the second half of the 1990s that the economy kicked into a higher gear. The 2001 recession did not have financial sector complications, but the employment recovery took much longer and private sector employment growth through the expansion was one of the worst ever. Capital spending remained depressed through the recovery. In fact, through the past 25 years, barring the Dotcom bubble phase, capex has never been robust.

To the extent the last thirty years appear to have delivered stability, it is because the economy has been operating under considerable slack the bulk of the time (see my post). Persistent slack has meant that the Fed has kept interest rates low for a extended periods of time but also that the feedback loops from balance sheets to the economy have been weak. As a result, rising asset prices or easy credit have failed to stoke the real economy commensurately, keeping interest rates low, supporting balance sheets, and fostering the perception of stability. In turn, this validated balance sheet structures and encouraged further risk taking. In other words, interest rates were not low enough for the real economy but too low to rein in financial market exuberance. However, with the passage of time, the feedback loops from balance sheets to economy strengthened--think wealth effects in the 1990s or home equity extraction in the 2000s--diminishing the slack. At that point, the relationship flipped. The interest rate high enough to stabilize the real economy was too high to stabilize collapsing balance sheets.

All this may sound incredibly nihilistic, but it is not. We need to reorient policy toward building a resilient system not chasing the unattainable goal of stability (see my post).

While I agree entirely with "We need to reorient policy toward building a resilient system", I think it's important to have a good understanding of the history in order to figure out what will make the system resilient. When I followed the link to your post on the socialization of risk you wrote: "every crisis has led to more, not less, socialization of risk over the past 200 years of western capitalism." This is a very dramatic claim that there is not well founded.

ReplyDeleteWestern capitalism was built on carefully calibrated (i.e. resilient) institutions, as I argue here: https://doi.org/10.1017/S0968565016000020 . Unless we choose to study and understand our history, we are unlikely to be able to achieve the goal of "resilience" that you proclaim.

Carolyn Sissoko

This comment has been removed by the author.

DeleteTo be more specific, your chart is excellent. But it's important to understand that the 19th century institutions that evolved in Britain -- and affected access to credit worldwide -- were designed to control the growth of credit (and in particular its effect on asset prices and economic activity) in addition to managing policy rates. Similarly after the reforms of the 1930s US institutions were also designed to limit the growth of credit -- though in a very different way, and probably less effectively than the British model.

DeleteThe credit cycle that Minsky was observing initially was often just a business cycle -- because credit growth was controlled. As the goal of controlling credit growth and its effects on asset prices and economic activity was forgotten, our institutions evolved to no longer perform this basic role -- and so we find ourselves experiencing a financial cycle that appears to be getting ever more destabilized over time.

Carolyn Sissoko

Will look into your book.

DeleteAnother thoughtful and thought-provoking post as usual, Srini. The last paragraph of the post has been the rallying cry of BIS economists from White to Borio (including Cecchetti or not?).

ReplyDeleteI found the paragraph on the 'ex-post criticism' of the Fed not being easy enough in mid-2008 to be particularly insightful. Hindsight is a gift for critics that is denied to policymakers in real time!

The blog post can be considered a formulation of 'Thiruvadanthai Trilemma' between free-market finance, financial stability and economic stability. You can have two of the three but not all of them.

Notice that I have taken interest rates out of this trilemma. That is deliberate. In other words, the problem that there is no one single interest rate that stabilises the financial economy and the real economy at the same time disappears if (a) we remove the paradigm that 'markets know best' particularly for the financial sector and for financial markets (in a sense, I believe, the comments by Ms. Carolyn Sissoko reflect that) and if (b) the relevant horizon to evaluate the correctness of the monetary plolicy setting was long enough.

In a long enough time horizon, the dilemma of fixing a rate that handles financial market exuberance that allegedly hurts real economic activity or a low enough rate that allows financial intermediation to repair or to resume while the economy is overheating solves itself.

In recent times, I beleive that the former dilemma has imposed much bigger long-run costs on the economy and on the society than the latter dilemma, in the above paragraph.

If unelected and technocratic policymakers optimise their decision over a reasonably long time frame, then the need for (or, the impossibility of) multiple policy rates is avoided or obviated.

If they cannot do that in practice that easily, then another approach is to have the domestic economy counterpart of 'unremunerated reserve requirements' that is applied to regulate capital flows. There can be a counter-cyclical credit surcharge (or discount) that the central bank, in its capacity as a banking regulator, prescribe for credit allocation, on the top of the policy rate. There can be times when this surcharge (negative or positive) can be zero. In that case, the policy rate works both for the financial economy and for the real economy. This can be on top of (and not in lieu of) countercyclical capital buffers that regulators now want to impose on banks.

Just my two cents worth.

The blog article very surprised to me! Your writing is good related to personal care In this I learned a lot! Thank you!, please checkout more information on Lotus Notes xpages Consultant

ReplyDeleteHello, everyone!! Are you looking for equity release? Don't worry! We are providing all the info after retirement. We waiting for you https://www.londonequityrelease.net.

ReplyDeleteThank you

This comment has been removed by the author.

ReplyDelete