As I wade into the Phillips curve debate, a voice in the back of my brain is saying, no. It is reminding me of a great couplet in a fantastic Bengali dystopian fantasy movie, Hirok Rajar Deshe (in the land of the diamond king), "The quest for knowledge is endless, (hence) the pursuit of knowledge is futile." Still, I persist.

Let us take stock of the main questions:

1. Is there a stable relationship between inflation and unemployment, as the Phillips Curve has been defined in recent times?

2. Is there a stable relationship between unemployment and wages, the original Phillips Curve?

3. Do wages cause inflation?

4. Ultimately, does unemployment cause inflation?

I am a firm believer in Jon Elster's dictum that explanation in social sciences means the identification of causal mechanisms. Inflation is caused by an increase in money supply is NOT such an explanation. Derivative ones of the idea such as the following: an increase in monetary base leads price setters to expect inflation and therefore set prices higher is also a useless mechanism. Have you ever come across a businessman that follows the monetary base and sets prices? The notion that money translates directly into inflation was dubbed Immaculate Inflation by Karl Smith.

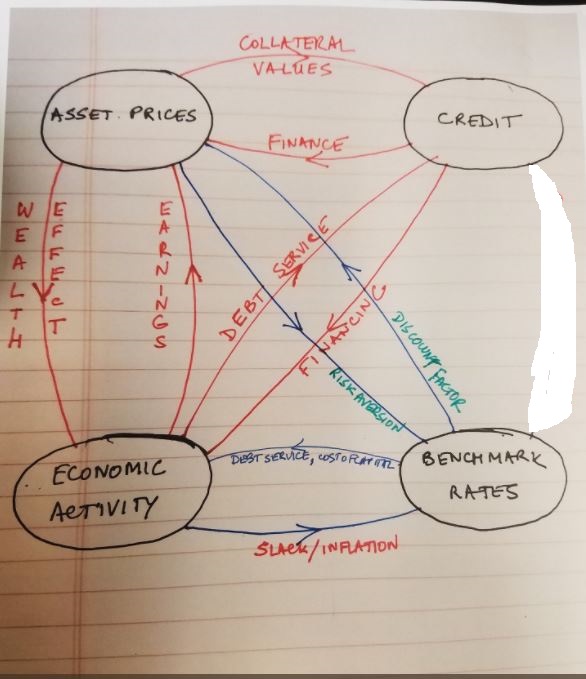

The following schematic represents the basic mechanism I have in mind, and I hope to show some evidence for it:

Here is a summary of my views:

Here is a summary of my views:

The following schematic represents the basic mechanism I have in mind, and I hope to show some evidence for it:

1. There is no stable Phillips Curve. There is a much better case for a wage Phillips curve than for a price Phillips curve.

2. The causality from unemployment to inflation runs through wages.

3. The relationship between unemployment and wages is nonlinear, context-dependent, and contingent on history and institutions.

4. There is a positive feedback loop between wages and prices, but the strength of that loop is also context dependent.

5. Yes, central banks have the power to interfere with these causal processes, but they are not omnipotent as Monetarists assume. Central banks face a trilemma: there is an inherent conflict in maintaining low unemployment, stable inflation, and financial stability (see my posts). The early postwar decades were an exception.

Let us start with wages and unemployment. Outside of coercive arrangements, is it outlandish to suggest that low unemployment will tend to drive wages higher? Of course, the context matters--the degree of unionization, the implicit compact between firms and workers (see for instance the excellent book The End of Loyalty), the degree of monopsony in labor markets, etc. Moreover, the unemployment rate might not be a good indicator of the slack in the labor market, as we have seen for much of this cycle. That said, in a fairly competitive, capitalist economy, the smaller the pool of available workers, the more difficult employers will find to fill open positions. More important, employers are likely to pay up to retain workers who may be lured away. Let us look at the evidence. The following is an excellent chart from a Cleveland Fed report:

As the chart shows, labor market slack has a stronger correlation with wages than with prices. In both cases, labor market slack leads--the correlations are much stronger when k is negative in the graph. To be sure, correlations have weakened in the post-1984 era. As I said, institutional context matters. Not only has unionization declined but also we have had extended periods of labor market slack in this era. As the chart below shows, the unemployment rate has been higher than the CBO's estimate of NAIRU for much of the post-1984 period.

Having shown some evidence for the first link, let us now turn to the wage-price link. In this case, there is a positive feedback loop: higher wages lead to higher prices, which in turn lead to demands for higher wages. Again, the context matters: for example the presence of institutional arrangements, such as cost-of-living-adjustments (indexation of wages to prices). Here is a chart that shows the employment cost index (ECI) against CPI services. I have used CPI-services ex-energy to isolate the prices of domestic nontradebles. In the tradeble sector, the ability of domestic producers to pass on cost increases will be constrained by competition from imports, especially in the era of global glut. Even a casual look at the chart shows that ECI leads CPI. I ran a crude two-way Granger causality test and the results reject the null hypothesis of no causality from wages to prices.

The Cleveland Fed paper, which runs the relationship between various wage measures and PCE, observes: "Our measures have been moderately positively correlated since 1960: both price inflation and wage inflation tend to be above (or below) trend at the same time (figure 2). The strongest correlations have been between core PCE inflation and the ECI. The weakest correlations have been with the CPH measure, which is not surprising given its volatility. Depending on the measure, wages either lead core PCE inflation very slightly or are contemporaneous with it: the correlation peaks come in quarter t+1 or t." They also note that the correlations have been weaker since 1980, which is to be expected given that there is widespread overcapacity in the domestic economy even outside the tradeable sector.

The usual Monetarist response is that the feedback loop between wages and prices would never get started unless the Fed accommodated the process by allowing money supply to increase. True, but the only way to curb the feedback loop is to weaken the real economy and the labor market. Immaculate control of inflation does not exist. Yes, expectations do matter, but more likely in the context of high inflation. At low levels of inflation, the expectations fairy is just that.

The bottom line: there may not be any stable Phillips curve but to infer that there is no relationship between labor market slack and inflation is not warranted.

Having shown some evidence for the first link, let us now turn to the wage-price link. In this case, there is a positive feedback loop: higher wages lead to higher prices, which in turn lead to demands for higher wages. Again, the context matters: for example the presence of institutional arrangements, such as cost-of-living-adjustments (indexation of wages to prices). Here is a chart that shows the employment cost index (ECI) against CPI services. I have used CPI-services ex-energy to isolate the prices of domestic nontradebles. In the tradeble sector, the ability of domestic producers to pass on cost increases will be constrained by competition from imports, especially in the era of global glut. Even a casual look at the chart shows that ECI leads CPI. I ran a crude two-way Granger causality test and the results reject the null hypothesis of no causality from wages to prices.

The Cleveland Fed paper, which runs the relationship between various wage measures and PCE, observes: "Our measures have been moderately positively correlated since 1960: both price inflation and wage inflation tend to be above (or below) trend at the same time (figure 2). The strongest correlations have been between core PCE inflation and the ECI. The weakest correlations have been with the CPH measure, which is not surprising given its volatility. Depending on the measure, wages either lead core PCE inflation very slightly or are contemporaneous with it: the correlation peaks come in quarter t+1 or t." They also note that the correlations have been weaker since 1980, which is to be expected given that there is widespread overcapacity in the domestic economy even outside the tradeable sector.

The usual Monetarist response is that the feedback loop between wages and prices would never get started unless the Fed accommodated the process by allowing money supply to increase. True, but the only way to curb the feedback loop is to weaken the real economy and the labor market. Immaculate control of inflation does not exist. Yes, expectations do matter, but more likely in the context of high inflation. At low levels of inflation, the expectations fairy is just that.

The bottom line: there may not be any stable Phillips curve but to infer that there is no relationship between labor market slack and inflation is not warranted.