A few days ago I tweeted about capitalism, fiat, gold, and cryptos. Seeing the comments, I realized the topic needed to be dealt with in long form. Essentially, the rise of capitalism has gone hand-in-hand with increasing socialization of risk--and this is not a mere coincidence. Central banking, fiat money, social insurance programs, and countercyclical fiscal policy are all intimately related to the expanded socialization of risk. Whether the greater socialization of risk is a moral/ethical is an impossible question that I don't want to get dragged into. Instead, I want to highlight the implications for investors:

1. Although the socialization of risk has had naysayers right from the beginning, every crisis has led to more, not less, socialization of risk over the past 200 years of western capitalism. Those betting on the ultimate collapse of the system--eg. gold bugs--would do well to remember this.

2. The nature of socialization has changed over the past thirty years--the era of inflation targeting and monetary policy dominance--which has profoundly changed the nature of business cycles and the statistical distribution of market outcomes.

Ha Joon Chang had an excellent op-ed in the Guardian several years ago briefly describing the history of the socialization of risk. Basically, starting with limited liability to deposit insurance, governments have enacted policies that attempt to put a floor on losses suffered by risk takers. In the parlance of finance, there is a government put on risky activity. Over time, the government put has expanded to establishing a floor on economic activity and financial markets. Central banking and automatic fiscal stabilizers are part of the expanded government put. The Gold Standard fundamentally interfered with this socialization by constraining governments' ability act in crises. Unsurprisingly, the Gold Standard fell by the wayside. Since Enlightenment, western countries have operated on the principle that man (woman) is the measure of all things and our job is to make life living on this earth (Orwell). It is our belief in our capacity to arrange our affairs and not leave it to providence that marks the radical departure from pre-Enlightenment. In that light, the gold standard is an anachronism--it denies the idea that human beings collectively can durably manage their affairs.

The moral distaste for socialization that some people have often leads them to the erroneous conclusion that such a system must fail, which is very rooted in a religious worldview. Yet such a view would serve an investor poorly.

Over the past thirty years, the nature of the government involvement has changed from establishing a floor to smoothing fluctuations. We have gone from crisis-fighting to promoting tranquility--that is, from selling a put to reducing vol. The original mandate of central banking was to act as a lender of last resort in financial crises. In the post-war era, it expanded to business cycle management. In the inflation targeting era, it has morphed into promising low volatility. Yet, the attempt to deliver low volatility--unlike the attempts to provide a floor--is self-defeating. By promising low and stable inflation, central banks have encouraged excessive leveraging. Credit investors are basically selling a straddle. If economic activity and inflation crater, they suffer losses. On the other hand, if economic activity and inflation are too hot they stand to lose as well, if not on an absolute basis at least on a relative basis. (If economic activity is strong but inflation is contained, then credit investors don't lose on an absolute basis but they fall behind equity investors.) Unsurprisingly, the inflation targeting era has witnessed explosive growth in private sector debt. Ironically, the real beneficiaries are equity investors and government bond investors. Credit investors are effectively selling a put option to the borrowers (equity holders). Lower the premium charged by credit investors, the cheaper the cost of a put for equity investors. Notwithstanding the promises of central bankers, there is a strong human tendency to overpay for lottery like payouts, which is why equity investors are loathe to give dilute their stake. Inflation targeting has made it only easier for equity holders to indulge in their biases.

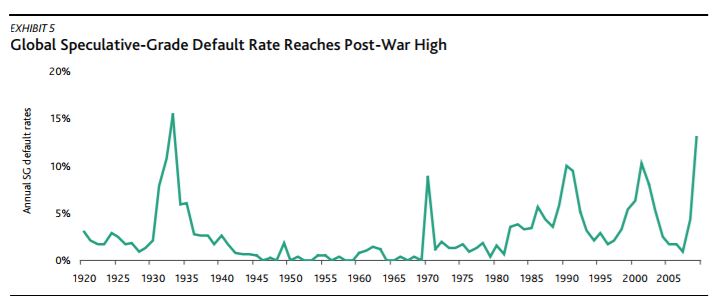

Meanwhile, the explosive growth in private sector debt makes the financial system unstable and prone to deflationary bias. Even as volatility of economic activity and inflation has gone down, the skew in financial markets has actually worsened in the past thirty years. (I would argue that the skew in economic activity has also worsened but it is harder to present strong statistical evidence.) Take S&P as reported earnings. Earnings declines during recessions have become progressively worse. The same with corporate bond defaults. As a result, each crisis has accentuated safe asset demand and forced the Fed lower and lower, helping T-bond investors.

As Minsky said, stability leads to instability. Ashwin Parameswaran used to maintain a terrific blog, Macroresilience, He has argued that policy should aim for resilience (which I like much better than the notion of anti-fragile) not stability. Meanwhile, stability is leading to rebirth of the CDO market.

1. Although the socialization of risk has had naysayers right from the beginning, every crisis has led to more, not less, socialization of risk over the past 200 years of western capitalism. Those betting on the ultimate collapse of the system--eg. gold bugs--would do well to remember this.

2. The nature of socialization has changed over the past thirty years--the era of inflation targeting and monetary policy dominance--which has profoundly changed the nature of business cycles and the statistical distribution of market outcomes.

Ha Joon Chang had an excellent op-ed in the Guardian several years ago briefly describing the history of the socialization of risk. Basically, starting with limited liability to deposit insurance, governments have enacted policies that attempt to put a floor on losses suffered by risk takers. In the parlance of finance, there is a government put on risky activity. Over time, the government put has expanded to establishing a floor on economic activity and financial markets. Central banking and automatic fiscal stabilizers are part of the expanded government put. The Gold Standard fundamentally interfered with this socialization by constraining governments' ability act in crises. Unsurprisingly, the Gold Standard fell by the wayside. Since Enlightenment, western countries have operated on the principle that man (woman) is the measure of all things and our job is to make life living on this earth (Orwell). It is our belief in our capacity to arrange our affairs and not leave it to providence that marks the radical departure from pre-Enlightenment. In that light, the gold standard is an anachronism--it denies the idea that human beings collectively can durably manage their affairs.

The moral distaste for socialization that some people have often leads them to the erroneous conclusion that such a system must fail, which is very rooted in a religious worldview. Yet such a view would serve an investor poorly.

Over the past thirty years, the nature of the government involvement has changed from establishing a floor to smoothing fluctuations. We have gone from crisis-fighting to promoting tranquility--that is, from selling a put to reducing vol. The original mandate of central banking was to act as a lender of last resort in financial crises. In the post-war era, it expanded to business cycle management. In the inflation targeting era, it has morphed into promising low volatility. Yet, the attempt to deliver low volatility--unlike the attempts to provide a floor--is self-defeating. By promising low and stable inflation, central banks have encouraged excessive leveraging. Credit investors are basically selling a straddle. If economic activity and inflation crater, they suffer losses. On the other hand, if economic activity and inflation are too hot they stand to lose as well, if not on an absolute basis at least on a relative basis. (If economic activity is strong but inflation is contained, then credit investors don't lose on an absolute basis but they fall behind equity investors.) Unsurprisingly, the inflation targeting era has witnessed explosive growth in private sector debt. Ironically, the real beneficiaries are equity investors and government bond investors. Credit investors are effectively selling a put option to the borrowers (equity holders). Lower the premium charged by credit investors, the cheaper the cost of a put for equity investors. Notwithstanding the promises of central bankers, there is a strong human tendency to overpay for lottery like payouts, which is why equity investors are loathe to give dilute their stake. Inflation targeting has made it only easier for equity holders to indulge in their biases.

Meanwhile, the explosive growth in private sector debt makes the financial system unstable and prone to deflationary bias. Even as volatility of economic activity and inflation has gone down, the skew in financial markets has actually worsened in the past thirty years. (I would argue that the skew in economic activity has also worsened but it is harder to present strong statistical evidence.) Take S&P as reported earnings. Earnings declines during recessions have become progressively worse. The same with corporate bond defaults. As a result, each crisis has accentuated safe asset demand and forced the Fed lower and lower, helping T-bond investors.

As Minsky said, stability leads to instability. Ashwin Parameswaran used to maintain a terrific blog, Macroresilience, He has argued that policy should aim for resilience (which I like much better than the notion of anti-fragile) not stability. Meanwhile, stability is leading to rebirth of the CDO market.

A thoughtful post, as usual. But, I think you need to flesh it out a bit more. Typos can also be fixed. But, that apart, there may also be a conflation of two issues. The socialisation of risk may be driven by many instincts. I am not even sure that it is a post-Enlightenment idea that humans must take charge of their affairs that has led to socialisation of risk. Is it not a phenomenon boosted by the Great Depression and reinforced by prosperity of the post-World War II years?

ReplyDeleteSecond, resistance to the socialisation of risk need not be religious. While your warning to gold bugs is interesting, it is true only if the belief in the collapse of socialisation of risk is rooted in theology or religion. If it is rooted in reason - i.e., if the belief - that it is not sustainable anymore - that does not invalidate gold bugs except that no one can safely predict the carrying capacity and willingness of the governments to continue with socialisation of risk. That uncertainty for gold bugs is only an extension of the uncertainty that investors and strategists who call a stock market top face.

Further, socialisation of risk could also be explained by the swing in the relative balance of power between capitalists and the rest whereby they secured gains for themselves while they convinced the government (and the central banks) intellectually (well, if it is a revolving door thing, then it does not need much intellectual persuasion - one can get in and write the rules oneself) that socialisation of risk is the right thing to do.

Simply put, the dating of the socialisation of risk and tracing its rationale to post-Enlightenment needs to be better grounded.

I would add that "our belief in our capacity to arrange our affairs and not leave it to providence" has engendered excessive risk taking and then, the humans (capitalists and their friends in governments and policymaking bodies or they themselves when they went into government) arranged for the socialisation of those risks with asymmetric right tailed distribution payoffs for themselves!

ReplyDeleteMmorpg Oyunlar

ReplyDeleteİnstagram takipci satın al

tiktok jeton hilesi

TİKTOK JETON HİLESİ

Sac ekim antalya

İnstagram Takipçi

instagram takipçi satın al

metin2 pvp serverlar

TAKİPCİ

PERDE MODELLERİ

ReplyDeletenumara onay

mobil ödeme bozdurma

nft nasıl alınır

ankara evden eve nakliyat

trafik sigortası

DEDEKTOR

web sitesi kurma

aşk kitapları

smm panel

ReplyDeletesmm panel

https://isilanlariblog.com

İnstagram takipçi satın al

hirdavatci burada

beyazesyateknikservisi.com.tr

SERVİS

tiktok para hilesi

pendik lg klima servisi

ReplyDeletebeykoz beko klima servisi

üsküdar beko klima servisi

pendik alarko carrier klima servisi

pendik daikin klima servisi

tuzla toshiba klima servisi

tuzla beko klima servisi

çekmeköy lg klima servisi

ataşehir lg klima servisi