Labor productivity in this expansion has been abysmal, with the last five years looking especially dreadful. Multifactor productivity has been slightly better, although it too has been anemic. Tyler Cowen thinks productivity is weak because Americans have become lazy and complacent. He has written a whole book about it. This would be not so egregious if productivity had also not dropped in the still-striving emerging markets. Maybe they too are becoming fat and happy. We all need to go back to the happy days of sweatshops perhaps to get our productivity juices flowing! leaving snark aside, most mainstream economists are puzzled. On the other hand, economists who think demand matters clearly recognize that the productivity slowdown has a lot to do with a persistently low-pressure economy. See, this EPI paper by Josh Bivens for an excellent exposition of the demand side view.

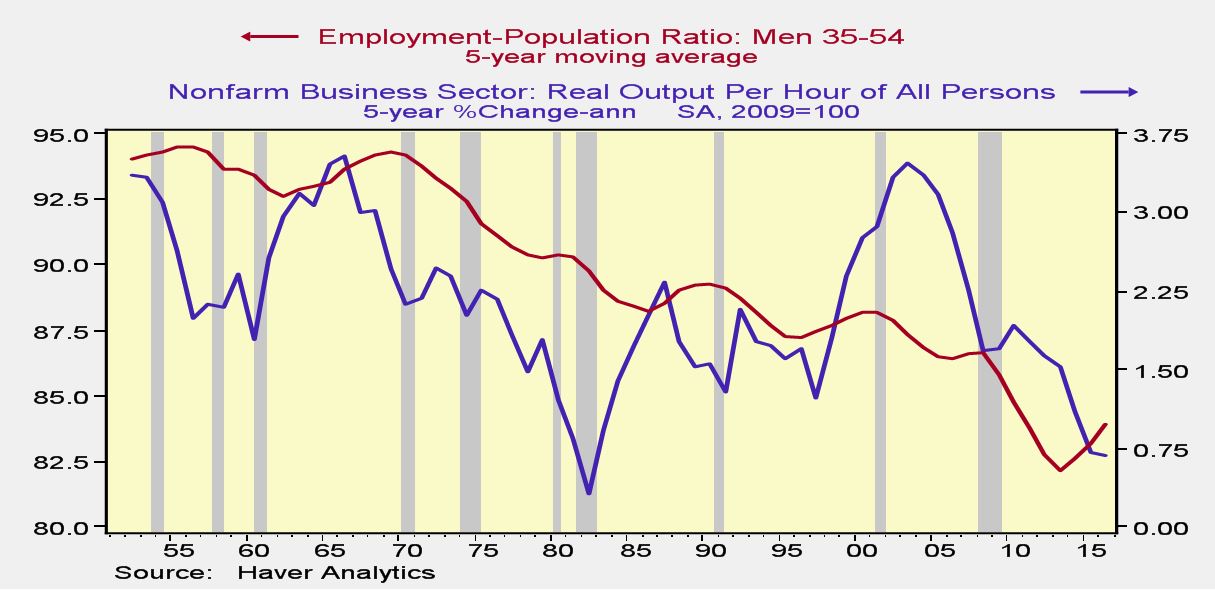

While I broadly agree with Josh Bivens, I have some disagreements about the causal factors. Bivens thinks that weak investment in new technology is hurting labor productivity, and tepid aggregate demand is keeping investment subdued. I agree on the latter point (see my exposition here). On the former point, I think Bivens understates his case by ignoring the direct impact of robust demand on productivity--the so-called Kaldor-Verdoorn law. The basic idea is that there are increasing returns to scale. I also think that a high-pressure economy that stretches its resources stokes people to find ways to use those resources more efficiently, raising productivity. There are two ways to see how productivity is related to utilization of resources. First, the trend in employment-population ratio for prime-age males has generally moved with the trend in productivity. (I have excluded 25-34 year-olds because more men are going to grad school. In any case, including them will not change the picture.) I don't think society has progressed to the point where 18% of prime-age men are now stay-at-home dads. Even if they are, it is likely because the prospects of a good job are poor and the cost of baby-sitting exceeds the jobs they might get. Essentially, this is a good proxy for labor market tightness in a secular sense.

Second, economywide capacity utilization has been weak on a secular basis (see my FT Alphaville post linked above). Business sector value added scaled to the capital stock--a proxy for economywide capcity utilization--co-moves with productivity, suggesting that utilizing existing capacity fully would increase productivity.

Bivens focuses on business sector investment as the culprit behind the slowdown in productivity. I want to focus on something that is in the hands of policymakers, government investment. Government investment is, surprise, closely related to productivity. We know that any causality has to run from the former to the latter because government decisions to invest are hardly driven by productivity in the overall economy! In particular, government investment in R&D has collapsed.

While I broadly agree with Josh Bivens, I have some disagreements about the causal factors. Bivens thinks that weak investment in new technology is hurting labor productivity, and tepid aggregate demand is keeping investment subdued. I agree on the latter point (see my exposition here). On the former point, I think Bivens understates his case by ignoring the direct impact of robust demand on productivity--the so-called Kaldor-Verdoorn law. The basic idea is that there are increasing returns to scale. I also think that a high-pressure economy that stretches its resources stokes people to find ways to use those resources more efficiently, raising productivity. There are two ways to see how productivity is related to utilization of resources. First, the trend in employment-population ratio for prime-age males has generally moved with the trend in productivity. (I have excluded 25-34 year-olds because more men are going to grad school. In any case, including them will not change the picture.) I don't think society has progressed to the point where 18% of prime-age men are now stay-at-home dads. Even if they are, it is likely because the prospects of a good job are poor and the cost of baby-sitting exceeds the jobs they might get. Essentially, this is a good proxy for labor market tightness in a secular sense.

Second, economywide capacity utilization has been weak on a secular basis (see my FT Alphaville post linked above). Business sector value added scaled to the capital stock--a proxy for economywide capcity utilization--co-moves with productivity, suggesting that utilizing existing capacity fully would increase productivity.

Bivens focuses on business sector investment as the culprit behind the slowdown in productivity. I want to focus on something that is in the hands of policymakers, government investment. Government investment is, surprise, closely related to productivity. We know that any causality has to run from the former to the latter because government decisions to invest are hardly driven by productivity in the overall economy! In particular, government investment in R&D has collapsed.

Merkur - xn--o80b910a26eepc81il5g.online

ReplyDeleteMerkur - 인카지노 Xn-o80b910a26eepc81il5g.Online. 메리트 카지노 고객센터 About this post. งานออนไลน์ Merkur. Xn-o-80b910a26eepc81il5g.Online. About this post. Merkur. Xn-o-80b910a26eepc81il5g.Online. About this post.