In my mind, the best example of applying MMT, while juggling structural inflation and balance of payments constraints, is India since 1980. Before I delve into the main story, a 5-minute tour of modern Indian economic history.

Until 1980, India was stuck in what was pejoratively termed the "Hindu rate of growth" by economist Raj Krishna. It is now widely acknowledged that growth took off in 1980, although in popular commentaries 1991 is seen as the watershed year. The chart below and more sophisticated tests show that there was a trend break in growth around 1980.

However, there is considerable debate about the causes of the growth takeoff in the 1980s and whether it was sustainable. Many, perhaps most, economists believe that the 1980s growth was unsustainable, fueled by a rapid increase in government spending and deficits. The deficit-spending spree led to a steep rise in government debt, rising inflation, and a worsening current account deficit and foreign currency debt culminating in the 1991 BOP crisis. The major dissenters from this view are the current CEA, Arvind Subramanian, and his co-author Dani Rodrik, who argued that the 1980s growth was not driven so much by old-fashioned Keynesian stimulus but by a more business-friendly attitude of the Indira Gandhi government.

Post-Keynesians predictably have a different take on the entire growth take-off story. Kevin Nell has a few papers arguing: 1) India was demand constrained in the 1952-1979 period, and fiscal expansion took the economy closer to potential; 2) India faced a BOP constraint on growth that was significantly eased by the surge in exports post 1991; 3) the post 1991 export surge may have had a demand-side explanation. I largely agree with Nell's analysis, although I disagree with him (and others) about how much the 1991 BOP crisis was the result of "unsustainable" growth in demand.

I am going to look at the India experience from the MMT angle of government deficits and sector financial balances. Since 1980, India has in effect followed the prescriptions of functional finance--generally pursuing fiscal and monetary policies that support high growth but turning attention to inflation-fighting and BOP concerns when needed. This strategy has actually allowed India to address poverty alleviation while delivering solid returns on capital (India has been one of the best in delivering dollar-based returns over the past 25 years).

Evolution of Fiscal Deficits

One of the most striking things about India was that the gross public sector deficit (the public sector includes the central and state governments, departmental enterprises, and public sector corporations; deficits are gross investment less gross saving) scaled to GDP has been permanently higher since 1980 (chart below). Only in one year, 2007-2008, did it fall below the peak of the pre-1980 range; in every other year since 1980, it has been higher than the peak of the pre-1980 range. Yet, this period has also coincided with the takeoff in the India's GDP from the previous Hindu rate of growth. One cannot establish that the deficits caused the growth ( I am working on a paper that seeks to establish this more formally--anyone interested in collaborating please email me), but such a chart has to warm MMT cockles.

At the same time, whenever faced with rising inflation, the government has throttled back. As the chart below shows, deficits have contracted whenever inflation has accelerated. This is straight out of the MMT playbook. The glaring error was in 2010, when deficits remained high despite surging inflation.

Meanwhile, government debt scaled to GDP has been relatively stable for nearly 30 years, except for the brief run-up in 2002-2003. Monetary policy may not have completely followed the prescriptions of functional finance, which is to conduct interest policy with a view to making debt sustainable, but it sure appears to have been doing something close.

One other point that supports the MMT view that government deficits are different from an expansion in money and credit brought about by private sector credit expansion. The Indian government nationalized 14 major banks in 1969 in order to make credit more widely accessible and to make "banks serve the needs of the nation." Nationalization appears to have been a factor in driving faster credit growth. M3 (which is a proxy for broad credit) scaled to GDP appears have had a trend break around 1969-1970, as the chart below shows. Yet, neither did GDP pick up nor did poverty decline in the 1970s.

The 1970s also illustrate the importance of supply side reforms to go along with demand push. In the 1970s, the government had terrible policies that hobbled the supply side: 1) harsh implementation of the monopolies and restrictive trade practices act that made plant sizes uneconomical and licenses hard to obtain, and 2) draconian controls that squelched imports of needed capital goods. Thus, inflation soared (of course, the oil shock of 1973 and poor monsoons aggravated matters). In the 1980s and much more so in the 1990s, the government eased supply-side constraints, allowing demand push to result in higher growth. Only demand push without supply side reforms would have been dissipated in higher inflation as in the 1970s.

Growth has been the Biggest Factor Driving Down Poverty

India has made remarkable progress in reducing the poverty rate over the past 35 years. The biggest factor driving the decline in poverty is economic growth, as the chart below shows. There was very little progress made in reducing poverty until 1980 despite the plethora of so-called poverty alleviation programs.

Return on Capital has also been Solid

Since 1995, in dollar terms, Indian stock market returns have almost matched the S&P 500 and handily beaten the world and other emerging markets.

I have argued elsewhere that Indian equities have also outperformed gold since 1979. Lastly, India's public provident fund (PPF)--a tax-advantaged small savings vehicle fully guaranteed by the central government--has outpaced gold and provided modest positive, real returns.

In short, India has not treated capital too shabbily.

Until 1980, India was stuck in what was pejoratively termed the "Hindu rate of growth" by economist Raj Krishna. It is now widely acknowledged that growth took off in 1980, although in popular commentaries 1991 is seen as the watershed year. The chart below and more sophisticated tests show that there was a trend break in growth around 1980.

However, there is considerable debate about the causes of the growth takeoff in the 1980s and whether it was sustainable. Many, perhaps most, economists believe that the 1980s growth was unsustainable, fueled by a rapid increase in government spending and deficits. The deficit-spending spree led to a steep rise in government debt, rising inflation, and a worsening current account deficit and foreign currency debt culminating in the 1991 BOP crisis. The major dissenters from this view are the current CEA, Arvind Subramanian, and his co-author Dani Rodrik, who argued that the 1980s growth was not driven so much by old-fashioned Keynesian stimulus but by a more business-friendly attitude of the Indira Gandhi government.

Post-Keynesians predictably have a different take on the entire growth take-off story. Kevin Nell has a few papers arguing: 1) India was demand constrained in the 1952-1979 period, and fiscal expansion took the economy closer to potential; 2) India faced a BOP constraint on growth that was significantly eased by the surge in exports post 1991; 3) the post 1991 export surge may have had a demand-side explanation. I largely agree with Nell's analysis, although I disagree with him (and others) about how much the 1991 BOP crisis was the result of "unsustainable" growth in demand.

I am going to look at the India experience from the MMT angle of government deficits and sector financial balances. Since 1980, India has in effect followed the prescriptions of functional finance--generally pursuing fiscal and monetary policies that support high growth but turning attention to inflation-fighting and BOP concerns when needed. This strategy has actually allowed India to address poverty alleviation while delivering solid returns on capital (India has been one of the best in delivering dollar-based returns over the past 25 years).

Evolution of Fiscal Deficits

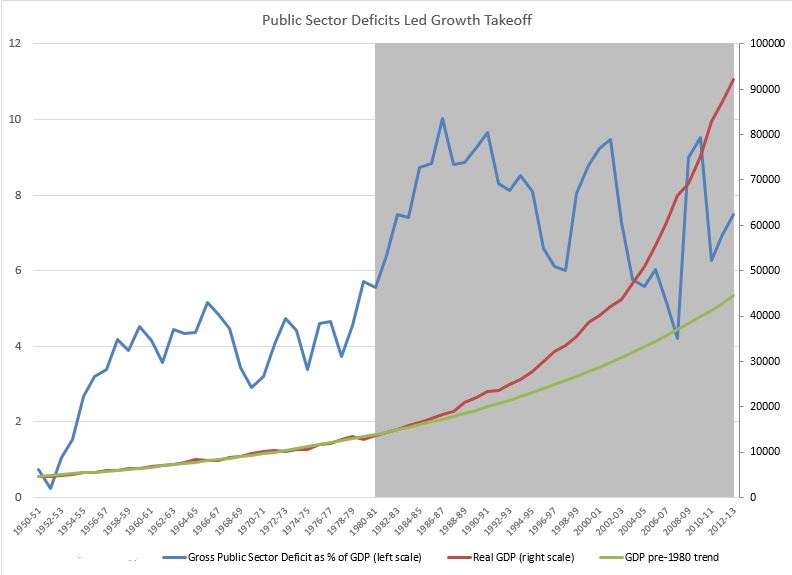

One of the most striking things about India was that the gross public sector deficit (the public sector includes the central and state governments, departmental enterprises, and public sector corporations; deficits are gross investment less gross saving) scaled to GDP has been permanently higher since 1980 (chart below). Only in one year, 2007-2008, did it fall below the peak of the pre-1980 range; in every other year since 1980, it has been higher than the peak of the pre-1980 range. Yet, this period has also coincided with the takeoff in the India's GDP from the previous Hindu rate of growth. One cannot establish that the deficits caused the growth ( I am working on a paper that seeks to establish this more formally--anyone interested in collaborating please email me), but such a chart has to warm MMT cockles.

At the same time, whenever faced with rising inflation, the government has throttled back. As the chart below shows, deficits have contracted whenever inflation has accelerated. This is straight out of the MMT playbook. The glaring error was in 2010, when deficits remained high despite surging inflation.

Meanwhile, government debt scaled to GDP has been relatively stable for nearly 30 years, except for the brief run-up in 2002-2003. Monetary policy may not have completely followed the prescriptions of functional finance, which is to conduct interest policy with a view to making debt sustainable, but it sure appears to have been doing something close.

One other point that supports the MMT view that government deficits are different from an expansion in money and credit brought about by private sector credit expansion. The Indian government nationalized 14 major banks in 1969 in order to make credit more widely accessible and to make "banks serve the needs of the nation." Nationalization appears to have been a factor in driving faster credit growth. M3 (which is a proxy for broad credit) scaled to GDP appears have had a trend break around 1969-1970, as the chart below shows. Yet, neither did GDP pick up nor did poverty decline in the 1970s.

The 1970s also illustrate the importance of supply side reforms to go along with demand push. In the 1970s, the government had terrible policies that hobbled the supply side: 1) harsh implementation of the monopolies and restrictive trade practices act that made plant sizes uneconomical and licenses hard to obtain, and 2) draconian controls that squelched imports of needed capital goods. Thus, inflation soared (of course, the oil shock of 1973 and poor monsoons aggravated matters). In the 1980s and much more so in the 1990s, the government eased supply-side constraints, allowing demand push to result in higher growth. Only demand push without supply side reforms would have been dissipated in higher inflation as in the 1970s.

Growth has been the Biggest Factor Driving Down Poverty

India has made remarkable progress in reducing the poverty rate over the past 35 years. The biggest factor driving the decline in poverty is economic growth, as the chart below shows. There was very little progress made in reducing poverty until 1980 despite the plethora of so-called poverty alleviation programs.

Return on Capital has also been Solid

Since 1995, in dollar terms, Indian stock market returns have almost matched the S&P 500 and handily beaten the world and other emerging markets.

I have argued elsewhere that Indian equities have also outperformed gold since 1979. Lastly, India's public provident fund (PPF)--a tax-advantaged small savings vehicle fully guaranteed by the central government--has outpaced gold and provided modest positive, real returns.

In short, India has not treated capital too shabbily.

India has also adopted another MMT favorite--job guarantee--in a limited way in the form of MNREGA. The present government has tried to ensure that MNREGA employment goes toward building assets in the form of rural infrastructure. (I am personally ambivalent about job guarantee.)

I am pretty sure that most Indian policymakers would be aghast to know that India has actually been following the prescriptions of MMT all along!

Good data. I'm on board with functional finance, but your poverty chart (as well as other sources) shows poverty declining since the mid 60's.

ReplyDelete.

Meanwhile, India's inequality started rising around 1980, or at best has not improved, depending on which metric you look at ( https://chartbookofeconomicinequality.com/wp-content/uploads/countrycharts/Static%20Images/static_png/India.png)

.

IMHO MMT has always been weak on the subject of inequality, or even completely apathetic.

"... IMHO MMT has always been weak on the subject of inequality, or even completely apathetic.... "

DeleteIt absolutely hasn't been 'apathetic'. To reach that conclusion you obviously have only taken a cursory glance at it, or simply not understood it.

Firstly, MMT is a monetary and macro *framework*, that provides the necessary *tools* to maximise output - ie use of real resources - and economic and price stability.

It's not, nor intended to be, a political manifesto. Inequality is a political choice.

However, MMT does provide a very powerful tool to redress inequality, directly affecting the share of returns to labour vs capital, depending on the extent to which politicians choose to use it. I'm referring to the Job Guarantee, you may have heard of it? (But if incapable of thinking in *macro* economics terms, like the vast majority of 'trained' economists, never mind the public, then you probably thought nothing of it.)

Thus, if politicians pick a shit wage and conditions for the JG, then it won't address inequality much. However, politicians could be elected who would choose a much higher level of JG income, and working conditions. I know, democracy is a shocking idea, huh? How lazy of us MMTers not to try and find a magic wand for you that would automatically read everyone's mind and automatically adjust to whatever average etc. was contained in the aggregate grey matter of each country?

As Bill Mitchell says, with good reason (tho' ignored by the cognitively incapable), the Job Guarantee is 'core' to MMT.

Of course, politicians could also choose a level of JG income that proves too high for too many businesses, and lags behind entrepreneurs capacity to start up more productive activities that can pay higher minimum wages. Then growth in productive capacity (the 'pie' to be shared) will also lag behind, and at some point wages growth will hit the real resources/inflation barrier. That's democracy. But the difference with an MMT informed electorate is that citizens will have the correct understanding of WHY the politicians screwed up, and just important, what the right *macro* steps are to improve matters.

@Mike, so anyone who criticizes MMT must be ignorant? It could not possibly be that MMT is flawed?

Delete.

I am well versed in MMT, thank you.

.

MMT is capitalism. MMT is neoliberalism with fiat money stirred in. It offers no unique tools.

.

*OF COURSE* politicians will pick a shit wage and conditions for any job program, in the unlikely event that a job program can even pass. Kalecki explained why that it so in 1943.

.

Yes, the JG is core to MMT and that is one of MMT's weaknesses, since the JG is flawed in numerous ways.

.

Even if you could pass a JG as MMT proposes it, it still would not make much of a dent in inequality because it would not address the mathematical cause of inequality -- the 1%, or more accurately the 10%. If you completely eliminated poverty with various programs (either transfers or job programs) that would not make a dent in inequality because it would not make a dent in the upper 10%. MMT does not want to go after the upper 10%, in fact, many MMTer's are part of the upper 10%. MMT is pro-capitalist, created and led by the affluent who condescendingly believe they know what is best for the poor and working class.

.

Democracy? There is no democracy. Capitalism is incompatible with democracy. MMT's "tools" do not change that.

I've made numerous proposals to directly and effectively progressively alter current distributional outcomes. www.moslereconomics.com

ReplyDeleteA GREAT SPELL CASTER (DR. EMU) THAT HELP ME BRING BACK MY EX GIRLFRIEND.

ReplyDeleteAm so happy to testify about a great spell caster that helped me when all hope was lost for me to unite with my ex-girlfriend that I love so much. I had a girlfriend that love me so much but something terrible happen to our relationship one afternoon when her friend that was always trying to get to me was trying to force me to make love to her just because she was been jealous of her friend that i was dating and on the scene my girlfriend just walk in and she thought we had something special doing together, i tried to explain things to her that her friend always do this whenever she is not with me and i always refuse her but i never told her because i did not want the both of them to be enemies to each other but she never believed me. She broke up with me and I tried times without numbers to make her believe me but she never believed me until one day i heard about the DR. EMU and I emailed him and he replied to me so kindly and helped me get back my lovely relationship that was already gone for two months.

Email him at: Emutemple@gmail.com

Call or Whats-app him: +2347012841542